|

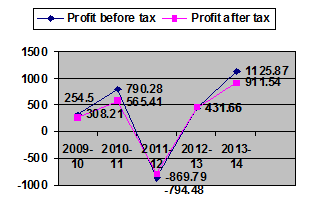

The profitability of the company has steadily increased over the period. SIL has a rare distinction of maintaining its profitability track record since inception and even during the downturn of the industry during late 90s, and even in 2008 global financial crisis although all its peers including TATA group reported red figures.

The loss during the year 2011-12 is due to sudden and unexpected ban imposed on Iron Ore mining by the Hon’ble Supreme Court in the Bellary-Hospet belt. This resulted in disruption to production of Iron and Steel products of this unit as well as other Iron and Steel making units in the belt whereby the production of other products viz., Metallurgical Coke and Power were also affected. This resulted in lower production and sales volumes. The unprecedented depreciation of Rupee vis-à-vis US dollar by almost 22% during the year also adversely affected the performance of the industry as well as this company. The high interest rates were another factor on account of which interest and finance costs have gone up significantly.

The company reported loss of Rs.869.79 million as against profit before tax of Rs.790.28 million a year before. The company made a smart recovery in FY 2012-13 by report profit before tax of INR 58 million in the face of adverse market conditions. The profit before tax is expected to rise to INR 431.66 million and INR 1124.87 million in 2012-13 and 2013-14 respectively in view of the full benefits of expansion of power generating capacity; benefits of backward and forward integration at its Pig Iron making plant. It may be mentioned that the co-generation power plant utilizing the waste heat (which otherwise would have to be let off into the air) and addition of thermal power will generate an income of over INR 1700 million and the profits there from are exempt from tax. In other words contribution from the co-generation power plant is expected to add to the profitability of the significantly.

The profitability forecast of the company is realistic and is achievable in view of the expected commissioning of the sinter plant, modernisation of blast furnace and Ductile Iron Pipe making plant apart from captive thermal power plant.

|